Cinda Futures: PTA is optimistic about the bargain-hunting layout

Client

Core view

Crude oil: The medium-term oil price has a reduction agreement. The bottom 50 US dollars/barrel support is difficult to break. However, the return of the US shale oil is expected to make the oil price rebound. The above 55 US dollars are suppressed by the shale oil producers, and the current fund is net. Positions are at a new high in six years, and the overall congestion will affect the upward pressure on oil prices to a certain extent. In February, oil prices will remain within the 50-55 range.

Naphtha: The price of refined oil and LPG is strong, driving naphtha prices stronger. The naphtha cracking spread will remain high before the end of the first quarter, and is expected to run in the range of 100-120 USD/ton.

PX: At present, the PX-naphtha price difference is running at a low level around 350 USD/ton. The PX price is seasonally weak in the first quarter, but the PX equipment maintenance is very strong in the second quarter of this year. The PX price may reflect the market maintenance expectation in advance, PX- The naphtha spread is expected to gradually increase. PTA: In the January-February 2017, the PTA inventory was about 250,000-300,000 tons. The inventory accumulation before and after the Spring Festival in the first two years dropped by about 100,000-1,500 tons. Compared with previous years, PTA supply pressure is not large.

Polyester: This year's Spring Festival polyester factory maintenance efforts are not as good as in previous years, and the situation of resuming work after the year is also significantly advanced, mainly due to the better profit of polyester finished products and the low inventory level. In addition, several sets of bottle tablets are expected in the first half of the first quarter. Will be put into production.

Overall, crude oil maintained range volatility, naphtha and PX prices are expected to be strong, and the cost side is expected to improve PTA; while PTA's own supply and demand enters seasonal off-season, but PTA inventory accumulation has fallen sharply compared with previous years, downstream The maintenance of polyester is significantly lower than in previous years, and the level of polyester inventories is also at a low level in recent years. The resumption of the polyester factory is also significantly advanced in the year.

Operation strategy: PTA will continue to see more before the end of April. It is recommended to refer to the PTA processing fee below 500. The current upstream price and processing fee are calculated. The TA1705 contract is below 5350, and the short-term target is around 5800. Loss 5200.

I. Review of PTA market in January 2017

Figure 1: PTA main market chart

Source: Wenhua Finance, Cinda Futures R&D Center

In January 2017, the PTA futures price showed a narrow range of fluctuations. First, the upstream crude oil fluctuated at a high level in January, and the price center of gravity fell slightly. The cost end basically framed the operating range of PTA. Secondly, the downstream polyester demand weakened in January, and the finished product cash flow also fell sharply in January. In the end, the low-level rebound in stocks and the weakening of downstream demand; finally, from the point of view of PTA itself, the PTA plant was basically fully loaded in January, the supply was sufficient, the PTA processing fee was maintained at a high level of 550, and the processing fee lacked upward momentum. . On the whole, in January, when PTA was driven by lack of cost and its supply and demand side was weak, it was more reasonable to maintain a narrow range of fluctuations.

Second, crude oil - PX-PTA-PET industry chain supply and demand analysis

(1) PET and terminal market analysis 1. Terminal internal demand is better than external demand

In December 2016, China's textile and apparel exports amounted to US$23.433 billion, an increase of 8.37% from the previous month and a decrease of 13.05% from the same period last year. Among them, the export value of textiles (including textile yarns, fabrics and products) was US$ 9.156 billion, down 6.67% year-on-year; the export value of clothing (including clothing and clothing accessories) was US$ 14.277 billion, down 16.70% year-on-year.

From January to December 2016, China's textile and apparel exports totaled US$267.62 billion, down 5.74% year-on-year, of which textile exports totaled US$106.138 billion, down 2.95% year-on-year; apparel exports totaled US$1,611.98 billion, down 7.45 year-on-year. %. However, the decline in the growth rate of export value was also affected by the depreciation of the Renminbi, which affected the statistical caliber. According to the statistics of Renminbi, the export of China's textile and apparel in 2016 was basically the same as that in 2015.

In terms of domestic demand, in December 2016, the retail sales of clothing, shoes, hats and knitted textiles above designated size in China was 162.9 billion yuan, an increase of 7.1% year-on-year.

In 2016, the retail sales of clothing, shoes and hats and knitted textiles above designated size was 144.3 billion yuan, an increase of 7% year-on-year.

Figure 2: Textile and apparel exports and growth rate

Source: Wind, Cinda Futures R&D Center

Figure 3: Retail sales and growth of clothing, shoes, hats and knitwear

Source: Wind, Cinda Futures R&D Center

2. Polyester profits fell sharply and stocks rebounded at a low level

However, since January 17th, the load on the terminal loom has declined, the demand for terminals has weakened, the production and sales of polyester have declined, and the polyester plant has continued to maintain high construction and supply is sufficient. In addition, the price of PTA and MEG is firm in January, and the industrial chain Profits are transferred upstream. Although the profit dropped sharply from December, as of January 20, the cash flow of polyester products remained positive, which was still significantly improved compared with the same period in the same period of 16 years. With the lowering of the load on the terminal looms, the production and sales of polyester continued to remain low. In January, the inventory of finished polyester products rebounded, and the average inventory days increased by about 5 days from the end of December, but it was still low compared with the same period last year. Inventory pressure is not big.

Figure 4: Polyester cash flow trend

Source: CCF, Cinda Futures R&D Center

3, polyester started better than the same period last year

Figure 5: Polyester Finished Goods Stock Index

Source: CCF, Cinda Futures R&D Center

Capacity release is concentrated in the first quarter

As of January 20, the polyester load is still maintained at a high load of 80%. Although the load will continue to decline before the year, this year's polyester factory maintenance is obviously less than in previous years, which is related to the current polyester stocks in the finished product cash flow. related. As far as the current polyester plant plan is concerned, by the end of the month, the polyester load will be at or below 74%, which is 8-10 percentage points higher than the same period of the previous year, which greatly eased the oversupply pressure of PTA during the Spring Festival.

Figure 6: Polyester unit load

Source: CCF, Cinda Futures R&D Center

From the 17-year plan for the production of polyester plants, in the first quarter, 500,000 tons of Sanfangxiang, 550,000 tons of Wankai, and 600,000 tons of pelleting equipment of Chengxing are expected to be put into production. If it is put into production, it will greatly push PTA. Demand, although the 900,000 tons of PTA plant in Sichuan Pengwei will be put into production in February, it still cannot meet the demand for polyester capacity increase.

Table 1: 2017 polyester production plan

Source: CCF, Cinda Futures R&D Center

(II) Analysis of supply and demand of PTA

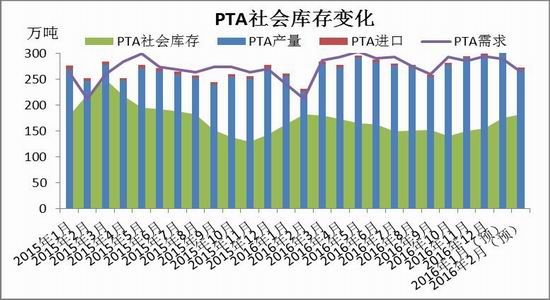

PTA enters the staged accumulation pool, but the magnitude is not as good as in previous years.

In January, the PTA devices that were inspected in the previous period were restarted one after another, basically at full load, but the polyester load remained high in the first half of January, so the PTA inventory was not obvious. In the second half of the month, the polyester plant began to concentrate and reduce the negative, while the PTA plant basically did not overhaul in January. The average PTA load in January was about 77.8% (the production base was 46.13 million tons), and the PTA output in January was about 3.05 million tons. The average monthly production of polyester is about 81.6%, the consumption of PTA is about 2.75 million tons, and the net export is about 30,000 tons. Considering the consumption of 80,000 tons of PTA in other fields, the overall supply of PTA in January is about 190,000 tons.

In February, Yisheng Ningbo set up a 2.2 million tons plant for parking and maintenance for half a month. Jialong 700,000 tons of equipment is also scheduled to stop in late February. In addition, Sichuan Pengwei 900,000 tons of equipment is also scheduled to resume production in February, such as There were no other unexpected situations. In February, the PTA output was about 2.68 million tons, the polyester output was about 2.95 million tons, and the PTA consumption was 2.545 million tons. Considering the net export and other areas of PTA consumption, it is estimated that the PTA oversupply in February is 7 About 10,000 tons.

Overall, in January and February 2017, PTA stocks totaled about 270,000 tons, which was a significant drop from the cumulative stock of 400,000 tons in January and February last year.

Figure 7: PTA dynamic supply and demand difference

Source: CCF, Cinda Futures R&D Center

Figure 8: PTA social inventory changes

Source: CCF, Cinda Futures R&D Center

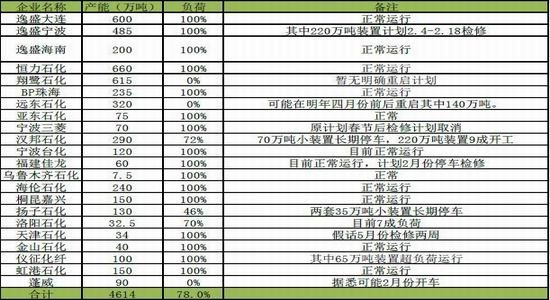

Table 2: Operation of PTA devices

Source: CCF, Cinda Futures R&D Center

(III) Cost-side analysis

1. PX processing fee is low, domestic inventory is basically stable

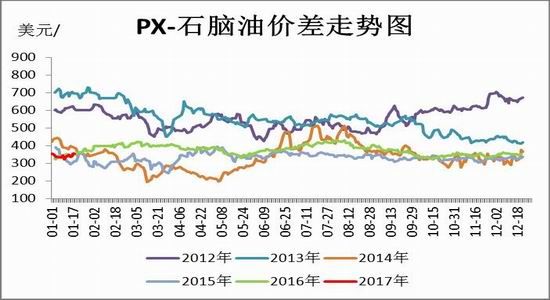

In January 2017, the price difference of PX-naphtha was low, and the average price difference was about 360 US dollars/ton. From the seasonal trend of PX-naphtha price difference, the PX processing trend in January-March was weak.

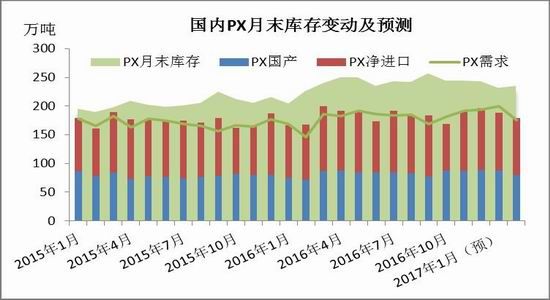

In January 2017, domestic PX stocks fell by about 100,000 tons, mainly due to the high load of PTA devices, driving the consumption of PX; entering February, Yisheng Ningbo 2.2 million tons and Jialong 700,000 tons devices have maintenance plans, PTA The load has declined from January. It is expected that the domestic PX inventory will increase in February, but the range is not large, about 30,000-50,000 tons.

Figure 9: PX-naphtha spread trend

Source: CCF, Cinda Futures R&D Center

Figure 10: Domestic PX Social Inventory

Source: CCF, Cinda Futures R&D Center

2. The maintenance of Asian PX devices in the second quarter is strong.

In the second quarter, it is usually the peak season for the maintenance of petrochemical plants. From the current point of view, the PX installations in Asia in the second quarter of 2017 involve an overhaul capacity of 8.6 million tons, accounting for 19% of the total capacity in Asia. The maintenance is huge, and 2015 and 2016 In the second quarter of the year, PX equipment maintenance capacity was 4.38 million tons and 4.52 million tons respectively. Under the circumstances that the maintenance of PX equipment is so huge, with the overlay of 900,000 tons of Pengwei and 1.4 million tons of equipment in the Far East, it is expected that the supply of PX in Asia will be severely tightened in the second quarter.

Table 3: Inspection of Asian PX installations in the second quarter of 2017

Source: CCF, Cinda Futures R&D Center

3. The price of naphtha remained strong in the first quarter.

In January 2017, the naphtha cracking spread rebounded from US$70/ton to US$100/ton. The main reason is seasonality. In the deep winter, the amount of heating oil (gas) increased greatly, and the price of LPG (liquefied petroleum gas) was sharp. Going higher, replacing naphtha for olefin production decline, boosting naphtha prices; in addition, domestic Christmas, as well as the Spring Festival to drive global gasoline consumption, gasoline prices are strong, naphtha used to increase oil consumption, promote Naphtha prices are rising. From the seasonal trend of naphtha cracking spreads, before March, the naphtha cracking spreads were seasonally strong.

Figure 11: Naphtha cracking spread

Source: CCF, Cinda Futures R&D Center

Figure 12: Gasoline-cloth oil spread

Source: CCF, Cinda Futures R&D Center

4, crude oil production cuts are basically in place

Figure 13: Naphtha-LPG spreads

Source: CCF, Cinda Futures R&D Center

The return of shale oil is expected to put oil prices under pressure

Judging from the current implementation process of reducing production in OPEC member countries, the overall performance is good. It is understood that Saudi Arabia, the United Arab Emirates, Kuwait and Qatar are all implementing production reduction agreements. Among them, Saudi Arabia’s crude oil output has fallen by at least 486,000 barrels per day to 100.58 million tons per day since January. Angola and Algeria have informed oil companies to cut crude oil production to meet their production cuts. Venezuela has implemented a commitment to reduce production by 95,000 barrels per day. Although Iraq’s exports hit a record high of 3.55 million barrels per day in December, the country has cut production by 160,000 barrels per day since the beginning of January, which has exceeded the three-quarters of the promised reduction of 210,000 per day. On the other hand, as the main representative of non-OPEC production cuts, Russian crude oil production has decreased by about 130,000 barrels per day from the post-Soviet record high of 11.25 million barrels per day in October last year, and has exceeded the monthly production cut of at least 50,000. The initial goal of the bucket/day. On the whole, the reduction of production at the moment of the oil-producing countries is basically in place. If these reductions can be confirmed by the data, it will undoubtedly be a positive signal, even if the oil-producing countries are only 80% complete by agreement, the crude oil market will also Return to balance at the beginning of 2017.

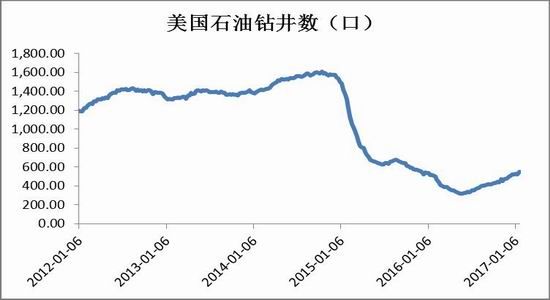

Although the implementation of the production reduction agreement is basically in place, the return pressure of the US shale oil still casts a shadow over the global oil market. In the week of January 20, the number of US oil drilling increased by 29 to 551, which is expected to be 1-3 months. It has a production capacity of 370,000 barrels per day.

Figure 14: Number of US oil wells

Source: CCF, Cinda Futures R&D Center

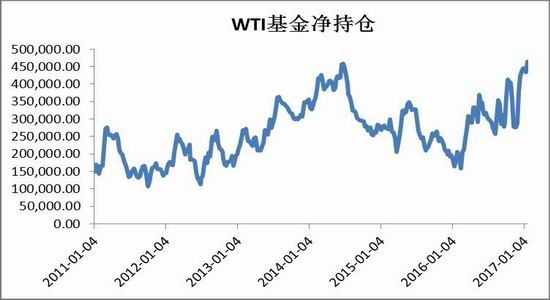

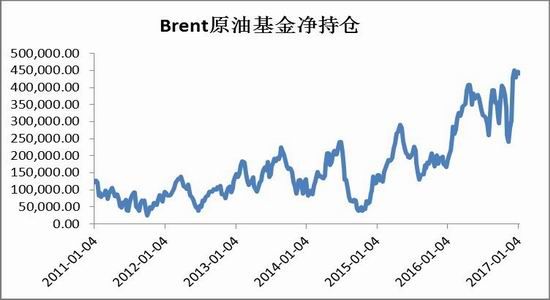

Near the end of the year, the CFTC's long position in the crude oil futures fund broke through the July 2014 high, a new high in six years. The overall crowded state will affect the upward pressure on oil prices to a certain extent.

Figure 15: WTI Fund Net Position

Source: CCF, Cinda Futures R&D Center

Figure 16: Brent Fund Net Position

Source: CCF, Cinda Futures R&D Center

Overall, the medium-term oil price has a reduction agreement, and the support below $50/barrel is difficult to break. However, the return of the US shale oil is expected to make the oil price rebound, and the oil price is also facing the shale oil producer's hedging suppression. In February, oil prices will remain dominated by the 50-55 range.

Third, the market outlook

Crude oil: The medium-term oil price has a reduction agreement. The bottom 50 US dollars/barrel support is difficult to break. However, the return of the US shale oil is expected to make the oil price rebound. The above 55 US dollars are suppressed by the shale oil producers, and the current fund is net. Positions are at a new high in six years, and the overall congestion will affect the upward pressure on oil prices to a certain extent. In February, oil prices will remain within the 50-55 range.

Naphtha: The price of refined oil and LPG is strong, driving naphtha prices stronger. The naphtha cracking spread will remain high before the end of the first quarter, and is expected to run in the range of 100-120 USD/ton.

PX: At present, the PX-naphtha price difference is running at a low level around 350 USD/ton. The PX price is seasonally weak in the first quarter, but the PX equipment maintenance is very strong in the second quarter of this year. The PX price may reflect the market maintenance expectation in advance, PX- The naphtha spread is expected to gradually increase. PTA: In the January-February 2017, the PTA inventory was about 250,000-300,000 tons. The inventory accumulation before and after the Spring Festival in the first two years dropped by about 10-15 million tons. Compared with previous years, PTA supply pressure is not large.

Polyester: This year's Spring Festival polyester factory maintenance efforts are not as good as in previous years, and the situation of resuming work after the year is also significantly advanced, mainly due to the better profit of polyester finished products and the low inventory level. In addition, several sets of bottle tablets are expected in the first half of the first quarter. Will be put into production.

Overall, crude oil maintained range volatility, naphtha and PX prices are expected to be strong, and the cost side is expected to improve PTA; while PTA's own supply and demand enters seasonal off-season, but PTA inventory accumulation has fallen sharply compared with previous years, downstream The maintenance of polyester is significantly lower than in previous years, and the level of polyester inventories is also at a low level in recent years. The resumption of the polyester factory is also significantly advanced in the year.

Operation strategy: PTA will continue to see more before the end of April. It is recommended to refer to the PTA processing fee below 500. The current upstream price and processing fee are calculated. The TA1705 contract is below 5350, and the short-term target is around 5800. Loss 5200.

Cinda Futures

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.

Yangzhou kennsi International Trade Co., Ltd. is a professional factory which is hammer at develop, produce and sale rope

It implements the business philosophy of [integrity management, customer first" and always provides customers with good products and technical support, sound after-sales service, and high-quality products.

Yangzhou YILIYUAN Rope & Net Factory , https://www.knsmy.com